Danger (Legal Disclaimer)

The information provided in this post is for purely informational and educational purposes. It does not constitute financial advice, investment advice, recommendation, or solicitation to buy or sell financial instruments.

- This content does not take into account your personal objectives, financial situation, or specific needs.

- Past performance does not guarantee future performance.

- Any investment carries risks, including partial or total loss of invested capital.

Your Banker, a Salesperson

Bank advisors are primarily salespeople subject to sales targets, not financial experts as one might believe. Their financial training is often limited, with many coming from professional reconversions. They are constrained by numerical objectives that strongly influence their recommendations, often to the detriment of the client’s interest. The increasing diversification of products offered by banks, ranging from insurance to mobile phone plans, further dilutes their already restricted financial expertise.

Commercial Objectives That Take Precedence Over Advice

At the beginning of each year, every bank advisor receives a list of numerical objectives to achieve: number of account openings, life insurance contracts, structured products to sell, etc. These objectives determine their annual bonus and condition their recommendations. An advisor who has already met their life insurance quota but not their structured products quota will tend to propose the latter to all their clients, regardless of their actual needs.

Commercial Diversification Remote from Financial Expertise

Driven by the search for PNB (Net Banking Product), equivalent to revenue, banks constantly diversify their offerings beyond traditional financial products. Advisors must now sell car insurance, home insurance, mobile phone plans, even home alarm systems. This forced versatility further dilutes their already limited financial expertise, as they have even less time to devote to understanding investment products.

Structured Products, Enemies of Performance

Structured products are often presented as sophisticated investment solutions, but this complexity primarily serves to mask their real costs and limitations. Even advisors often struggle to understand and explain these products in detail—test them, for example by asking about the product’s underlying index or bond allocation. Additionally, banks generally operate in a “closed architecture”, limiting investment options to internal products only, which severely restricts the choices available to clients.

Another major problem with structured products concerns the presentation of their performance. The displayed returns are often not annualized, making any honest comparison with stock indices impossible. This misleading presentation allows masking weak performance.

The ETF Alternative Neglected by Banks

ETFs (Exchange-Traded Funds), which allow diversified market exposure at low cost, are rarely proposed by bank advisors—when they know about them. This lack of knowledge is not trivial: ETFs often represent a more efficient alternative to structured products and actively managed funds that banks prefer to sell due to their higher margins.

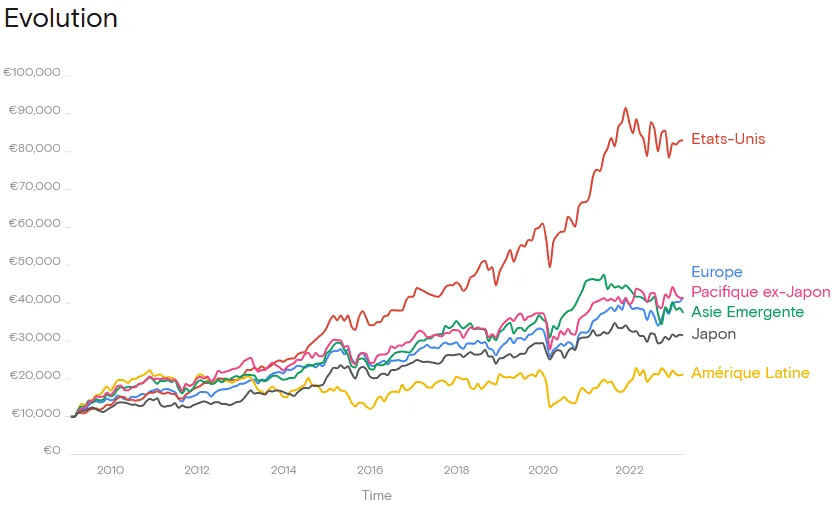

According to the SPIVA study, the reference in investment, 97-98% of active managers underperform the S&P 500 over a 20-year horizon.

Note

The SPIVA study concerns the S&P 500 index, meaning the 500 American companies with the largest market capitalization. Historically, the American market greatly outperforms the European market.

This statistical reality deeply questions the added value of active management promoted by banks, whether performed internally or by prestigious external managers like Morgan Stanley or Rothschild.

ETFs offer much lower fees than managed (or active) management and are by nature diversified (containing stocks from multiple companies, possibly across multiple countries).

Conclusion

- Your banker is often more salesperson than finance specialist. They must meet annual sales targets and sell internal products (they even get benefits in kind for performing :)

- Active management statistically underperforms the market (97-98% of active managers underperform the S&P 500 over 20 years).

- ETFs, often more efficient, are rarely proposed by banks.

- Educate yourself and invest first in your knowledge!

Sources

https://www.spglobal.com/spdji/en/research-insights/spiva/

https://blog.nalo.fr/produits-structures-performants/

To Go Further

The excellent Finary channel: